Strait of Hormuz and Global Energy Security: A Systemic Risk Exposed

Télécharger et lire la version française (PDF)

Introduction

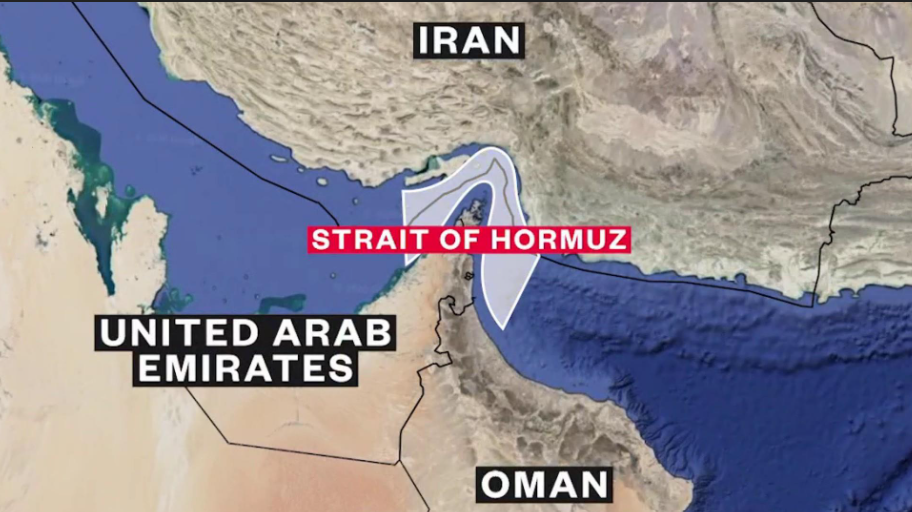

The Strait of Hormuz occupies a singular position in the global economic and geopolitical architecture. Its narrowest point, measuring roughly 33 km between Iran and Oman, makes it a strategic chokepoint through which nearly 20 million barrels of oil transit every day—around 20 percent of global consumption. Such a concentration of flows, originating from Iraq, Kuwait, Saudi Arabia, or the United Arab Emirates and destined for the rest of the world, would already be risky under normal circumstances. It becomes explosive when armed conflict turns the area into an unprecedented hotspot of tension. The impact would be immediate, affecting not only the security of maritime passage but also a global economy already weakened by successive crises. Past episodes of regional instability show that even a slight deterioration in conditions in the Gulf is enough to trigger a surge of several dozen dollars in the price of a barrel of oil (IEA, 2024). A prolonged conflict could therefore not only drive a sustained increase in global oil and gas prices but also fuel a new wave of inflation weighing on global growth. Ignoring this reality would constitute a major strategic error.

Escalation in 2026: A New Phase of Vulnerability

The recent strikes carried out by the United States and Israel against the Islamic Republic of Iran on 28 February 2026 have made the strait more vulnerable than ever, especially as they have triggered a dynamic of confrontation now spreading across the entire Middle East. This escalation was immediately reflected in market behavior: the price of WTI, which hovered around USD 67 per barrel in mid-February, reached its highest level in nearly five months before continuing its upward trajectory to close at roughly USD 91 on 6 March. Energy markets have already priced in a substantial risk premium, anticipating a continued rise in oil prices as well as higher maritime insurance costs in the months ahead. If no compromise is reached, this trajectory could intensify further, amplifying pressures on global energy markets.

Global Supply Chain Exposure and Economic Risks

The heightened market sensitivity stems from the fact that disruptions in the Strait of Hormuz—whether delays, attacks on tankers, or temporary restrictions—typically destabilize global supply chains for crude oil, refined products, and liquefied natural gas. Asian economies, heavily dependent on Gulf energy supplies, are the first to be exposed, but no region is truly insulated, given the increasingly global nature of energy interdependence. In a world where energy remains the backbone of industry, transport, and logistics, a sustained surge in hydrocarbon prices could quickly translate into a global economic slowdown.

According to IMF simulations (2024), a severe oil shock can shave several tenths of a percentage point off global GDP growth over a one to two-year horizon, while worsening external imbalances in net energy-importing countries. Emerging economies dependent on hydrocarbon imports—particularly in parts of Asia, the Middle East, Africa, and Latin America—would be especially vulnerable, facing a combination of price shocks, currency pressures, and fiscal strain (World Bank, 2024). With Middle Eastern conflicts already identified as one of the main downside risks to global growth, the current crisis would amplify existing fragilities. The consequences could be severe for major importing powers—from the United States and Japan to China and Europe—which lack credible short-term alternatives. Low-income countries, heavily dependent on global commodity prices, would not be spared. Such dependence creates an asymmetric power dynamic in which a few kilometres of water can influence the economic health of entire continents.

The Unequal Burden on Low‑Income Countries and the Mandate of International Institutions

Although all economies would be affected by a prolonged energy shock, low-income countries would remain the most fragile: in some of them, energy expenditures already exceed 10 percent of GDP. In this context, the role of the IMF and the World Bank becomes critical. The IMF must strengthen its multilateral surveillance, refine its stress testing models for oil shocks, and prepare emergency financing lines for the most exposed economies. The World Bank, for its part, must accelerate financing for the energy transition—given that nearly 80 percent of low-income countries still rely predominantly on imported fossil fuels—while supporting vulnerable states through reinforced social safety nets to cushion the impact of sustained price increases. Faced with multiplying energy shocks and rising financial vulnerability among importing countries, these institutions can no longer limit themselves to diagnostics: they must act preventively to ensure that a prolonged shock does not evolve into a generalized economic crisis.

Policy Responses: From Crisis Management to Strategic Diversification

Policy-makers also bear direct responsibility for managing this type of systemic shock. In the short term, they must coordinate the use of strategic reserves—representing an average of 90 days of imports for OECD countries—secure maritime routes, and limit panic-driven market reactions. In the medium term, the only genuine protection lies in diversification: diversification of energy sources, supply routes, and the energy mix itself, in a context where more than half of global oil trade passes through a handful of highly vulnerable maritime chokepoints. As long as the world remains heavily dependent on Gulf oil—which accounts for nearly one third of global crude exports—every crisis in the Middle East will become a global threat. The current conflict should serve as an electric shock, a stark reminder that energy security is not a technical issue reserved for specialists but a pillar of global economic stability.

Conclusion

The war in the Middle East underscores that energy security is not merely a sectoral concern but a central determinant of the international economic order (Hamilton, 1983). Beyond the immediate management of this crisis, one reality remains difficult to ignore: the global economy still rests on highly vulnerable transit points and unstable geopolitical equilibria. The Strait of Hormuz is not just a maritime corridor but a genuine stress test for the resilience of the international economic system, concentrating a critical share of global hydrocarbon trade. If international financial institutions and governments fail to act swiftly and in a coordinated manner—by securing flows, stabilizing markets, and reinforcing macroeconomic support mechanisms—the current crisis could become the trigger for a global slowdown whose effects would be felt for years.